Français

Français  Deutsch

Deutsch  Español

Español  Italiano

Italiano  Nederlands

Nederlands  Português

Português  Brasileiro

Brasileiro  Ελληνικά

Ελληνικά  Polski

Polski  Română

Română  Svenska

Svenska  Türkçe

Türkçe  Български

Български  हिंदी

हिंदी

Why Low Liquidity Increases Cost on Exchanges

Explains hidden costs and wider spreads in low-liquidity markets.

Novaxbet Editorial •2026-03-11•7 min read

Low liquidity is one of the most important structural factors influencing cost on a betting exchange. While many participants focus primarily on commission rates, the true economic cost of trading or betting often comes from the liquidity conditions of the market itself.

Liquidity determines how easily positions can be entered or exited without significantly affecting price. When liquidity is abundant, orders can be executed efficiently and prices remain stable. When liquidity is limited, even relatively small orders can move the market, increasing the effective cost of participation.

Understanding liquidity is therefore essential for interpreting exchange markets correctly.

What Liquidity Means on a Betting Exchange

Next reading

Liquidity refers to the amount of money available to be matched at different price levels within a market.

On a betting exchange, participants place back and lay offers into an order book. These offers form the pool of liquidity available for matching.

Higher liquidity means:

- more money available at each price level

- tighter spreads between back and lay prices

- greater stability when orders are executed

Lower liquidity means:

- less money available to absorb trades

- wider spreads

- greater price movement caused by individual orders

Liquidity therefore determines how smoothly a market functions.

Market Depth and Order Books

Liquidity is not only about the amount of money available at the best price. It also includes the depth of available liquidity across nearby price levels.

An order book shows how much money is available to be matched at different odds.

Example: Deep Market

| Odds | Available to Back |

|---|---|

| 2.00 | €45,000 |

| 1.99 | €40,000 |

| 1.98 | €36,000 |

In this environment, even large orders can be executed with minimal price movement.

Example: Thin Market

| Odds | Available to Back |

|---|---|

| 2.00 | €200 |

| 1.98 | €150 |

| 1.94 | €120 |

Here, even modest orders quickly remove liquidity and push the market to different prices.

Depth determines how resilient a market is to trading activity.

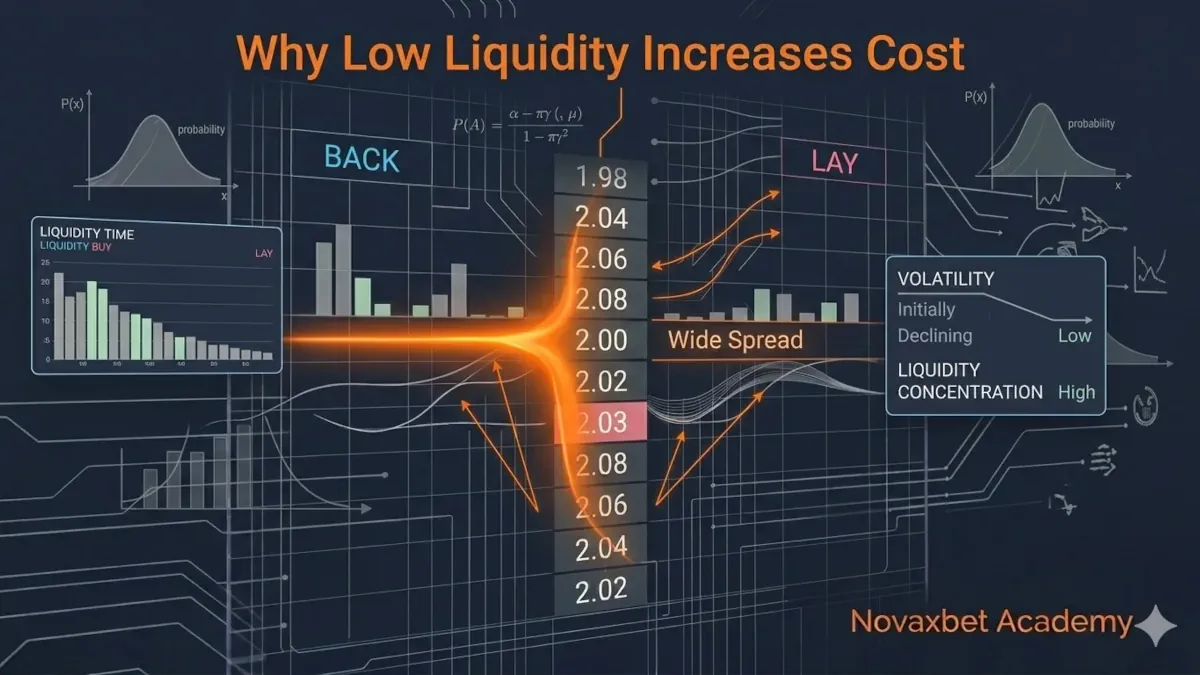

Spread: The First Cost of Low Liquidity

The spread is the difference between the best available back price and the best available lay price.

Example:

- Best Back: 2.02

- Best Lay: 2.10

Spread = 0.08

In highly liquid markets, spreads are typically narrow because many participants compete to provide prices.

Example of a tight spread:

- Back: 1.95

- Lay: 1.96

Spread = 0.01

In low-liquidity environments, spreads widen because fewer participants are willing to provide opposing offers.

A wider spread increases the cost of entering and exiting positions.

Execution Slippage in Thin Markets

Low liquidity also increases the likelihood of slippage, which occurs when orders are matched at worse prices than expected.

When insufficient liquidity exists at the best available price, orders must continue matching at the next available price levels.

Example

Market shows:

| Odds | Available |

|---|---|

| 2.00 | €150 |

| 1.98 | €120 |

| 1.95 | €90 |

A participant submits a €500 back order.

Execution occurs as follows:

- €150 matched at 2.00

- €120 matched at 1.98

- €90 matched at 1.95

- Remaining amount matched even lower

The final average price becomes significantly worse than the expected entry price.

This difference represents hidden cost created by low liquidity.

Volatility Amplification

Low liquidity markets are also more volatile.

In deep markets, large orders are absorbed gradually because substantial liquidity exists at multiple price levels.

In thin markets, even small orders can remove large portions of the order book.

This causes rapid price movement.

Example:

- Market price: 2.10

- Large order removes liquidity at 2.10 and 2.14

- Next available price: 2.20

The price jump occurs not because probability changed dramatically, but because liquidity disappeared.

Price movement in these cases reflects structural imbalance rather than new information.

Liquidity and Market Efficiency

Market efficiency improves when liquidity increases.

High liquidity markets benefit from:

- more participants

- greater information flow

- faster correction of mispricing

- stronger competition between traders

As liquidity grows, prices tend to converge toward consensus probability.

In low-liquidity markets, inefficiencies persist longer because fewer participants are actively correcting prices.

This creates opportunities, but also greater uncertainty and execution risk.

Hidden Costs Beyond Commission

Many users compare exchanges primarily based on commission percentages.

However, structural trading costs often exceed commission.

Example:

Two exchanges both charge 2% commission.

Exchange A: highly liquid market

Exchange B: low liquidity market

On Exchange A:

- spread = 0.01

- minimal slippage

On Exchange B:

- spread = 0.07

- slippage frequent

Even with identical commission, the effective cost of trading is significantly higher in the second environment.

Liquidity therefore acts as an invisible transaction cost.

Timing and Liquidity Cycles

Liquidity in exchange markets changes over time.

Most markets pass through predictable phases.

Early Market Phase

- opens hours or days before the event

- low liquidity

- wide spreads

- higher volatility

Growth Phase

- participation increases

- liquidity improves

- spreads narrow

Pre-Event Phase

- maximum liquidity

- stable prices

- efficient execution

For many markets, the majority of liquidity appears shortly before the event begins.

Understanding this cycle helps participants choose when to trade.

Large Orders and Market Impact

Participants placing large orders must consider market impact.

In low-liquidity environments, large orders can move price significantly.

Example:

Trader attempts to place a €5,000 order in a market where total visible liquidity is €1,200.

The order will consume multiple price levels and move the market substantially.

This results in:

- worse average price

- increased exposure to volatility

- visible market signals to other participants

Professional participants often split large orders into smaller pieces to reduce market impact.

Liquidity Providers vs Liquidity Takers

Two types of participants influence liquidity conditions.

Liquidity Providers

- place passive orders in the order book

- supply available prices

- improve market depth

Liquidity Takers

- execute against existing orders

- remove liquidity from the market

- cause price movement

Balanced markets require both.

When providers withdraw liquidity, spreads widen and price stability decreases.

Why Liquidity Concentrates in Major Markets

Liquidity tends to concentrate in markets with:

- popular sports or leagues

- high public interest

- strong professional participation

- large global audiences

Examples include:

- major football leagues

- Grand Slam tennis matches

- high-profile boxing events

Smaller competitions often remain structurally thin because fewer participants contribute liquidity.

Structural Risk in Low-Liquidity Markets

Low-liquidity markets expose participants to several structural risks:

- higher spreads

- increased slippage

- rapid price swings

- limited ability to exit positions

These factors can transform otherwise profitable strategies into losing ones due to execution inefficiency.

Understanding liquidity conditions is therefore as important as predicting event outcomes.

Liquidity as the Foundation of Exchange Markets

Betting exchanges function as marketplaces where price discovery emerges through interaction between participants.

Liquidity determines how effectively that marketplace operates.

Deep liquidity creates:

- efficient pricing

- narrow spreads

- stable execution

Thin liquidity creates:

- unstable prices

- higher trading costs

- unpredictable execution outcomes

For participants seeking long-term profitability, understanding liquidity is not optional.

It is one of the fundamental mechanics that shape every exchange market.