Français

Français  Deutsch

Deutsch  Español

Español  Italiano

Italiano  Nederlands

Nederlands  Português

Português  Brasileiro

Brasileiro  Ελληνικά

Ελληνικά  Polski

Polski  Română

Română  Svenska

Svenska  Türkçe

Türkçe  Български

Български  हिंदी

हिंदी

Exchange Commission vs Bookmaker Margin

Structural comparison between commission-based and margin-based pricing models.

Novaxbet Editorial •2026-03-15•5 min read

When comparing betting exchanges with traditional bookmakers, one of the most important structural differences lies in how costs are built into the system.

At first glance both platforms appear to charge a fee for participation. However, the way these costs are applied is fundamentally different.

Bookmakers incorporate their profit directly into the odds through a margin, while betting exchanges charge a commission on net winnings.

Understanding this distinction is essential because it explains why exchange markets often display more competitive pricing and greater transparency.

The Bookmaker Margin

Next reading

Traditional bookmakers earn revenue through what is known as the margin, often referred to as the overround.

This margin is embedded directly into the odds offered to customers.

In an ideal theoretical market with no margin, the implied probabilities of all outcomes would sum to exactly 100%.

However, bookmakers deliberately set odds so that the total implied probability exceeds 100%.

The excess represents the bookmaker’s built-in profit.

Example

Consider a football match with two possible outcomes.

| Outcome | Fair Odds | Bookmaker Odds |

|---|---|---|

| Team A | 2.00 | 1.91 |

| Team B | 2.00 | 1.91 |

Fair probability:

- Team A: 50%

- Team B: 50%

Total = 100%

Bookmaker implied probability:

- Team A: 52.36%

- Team B: 52.36%

Total ≈ 104.72%

The additional 4.72% represents the bookmaker’s margin.

Even if bets are perfectly balanced, this structure guarantees long-term profitability for the bookmaker.

Hidden Cost of the Margin

The bookmaker margin is embedded within the price itself.

This means participants do not see the cost directly.

Instead, the price they accept is already slightly worse than the true probability would justify.

Over time, this difference compounds.

For frequent bettors, the cumulative impact of margin significantly affects long-term returns.

Because the margin is built into every price, the cost applies regardless of whether a participant wins or loses.

The Exchange Commission Model

Betting exchanges operate under a different economic structure.

Instead of embedding profit into prices, exchanges charge a commission on net winnings.

Participants trade directly with each other:

- one participant backs an outcome

- another participant lays the same outcome

The exchange simply facilitates the transaction.

It does not take a directional position on the event.

Because of this structure, odds on exchanges often reflect closer approximations of true probability.

Example of Exchange Commission

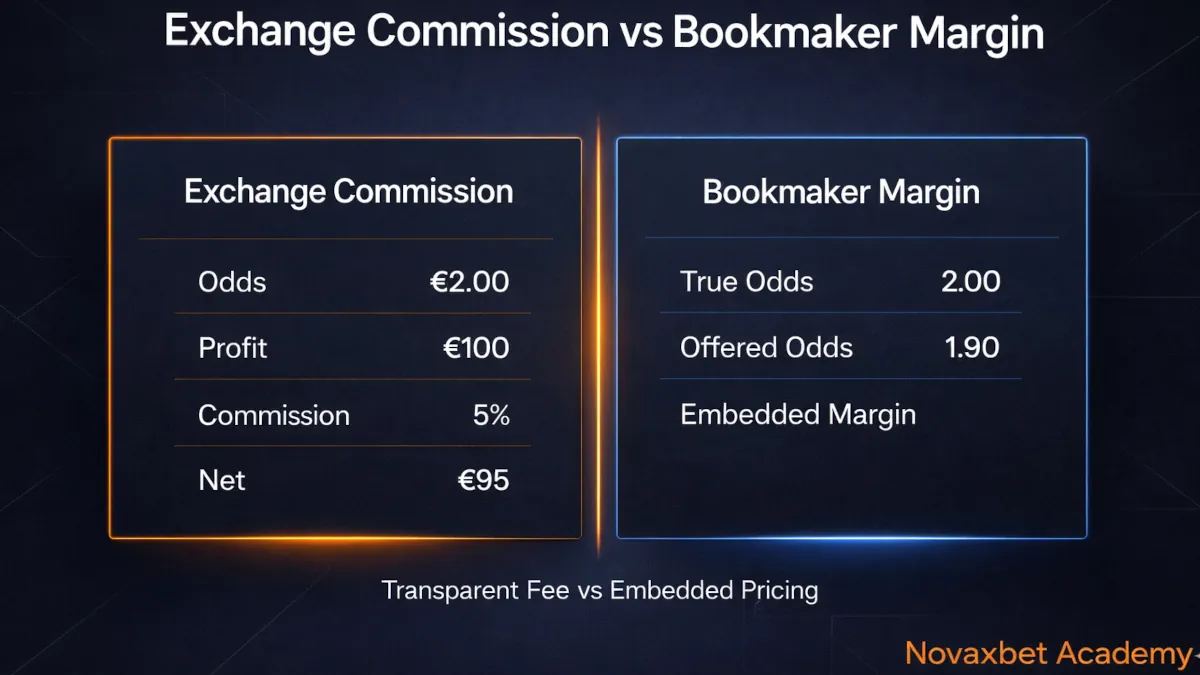

Suppose a participant backs an outcome at odds of 2.00 with a €100 stake.

If the bet wins:

- Gross profit = €100

- Exchange commission (5%) = €5

- Net profit = €95

If the bet loses:

- Stake lost = €100

- Commission = €0

Commission is only applied to winning outcomes.

This differs fundamentally from bookmaker margins, which apply to every bet implicitly through price.

Price Competition in Exchanges

Since exchange participants set their own odds, competition naturally pushes prices toward fair value.

Participants who offer unattractive prices are quickly undercut by others willing to provide slightly better odds.

This process leads to:

- tighter spreads

- improved price discovery

- lower effective market cost

Liquidity providers compete to attract trading volume.

As liquidity increases, pricing efficiency improves.

Transparency of Cost

Another key difference is cost visibility.

In bookmaker markets:

- margin is hidden within the odds

- participants rarely know the exact percentage being charged

In exchange markets:

- commission is explicitly stated

- participants can calculate the exact cost of trading

This transparency allows traders to evaluate strategies more precisely.

It also makes it easier to compare the true cost of different platforms.

Market Efficiency and Pricing

Exchange pricing often approaches fair probability more closely than bookmaker pricing.

There are several reasons for this:

- large numbers of participants contribute liquidity

- professional traders arbitrage inefficient prices

- competition forces continuous adjustment

Bookmakers, by contrast, adjust prices not only for probability but also to manage risk and exposure.

This means bookmaker odds may diverge from true probabilities.

Structural Incentives

The economic incentives of bookmakers and exchanges differ significantly.

Bookmaker Incentive

Bookmakers profit from imbalanced customer behavior.

Their objective is to manage risk and maintain profitable margins regardless of outcomes.

Prices are adjusted to:

- attract balanced betting

- reduce exposure

- maintain margin protection

Exchange Incentive

Exchanges profit from transaction volume.

Because commission is taken only from net winnings, exchanges benefit when:

- trading activity increases

- markets remain liquid

- participants continue interacting

This creates an environment where the platform’s incentive is to maintain efficient and active markets.

Comparing Long-Term Cost

Although exchange commission appears explicit and visible, the effective long-term cost is often lower than bookmaker margin.

Example comparison:

| Platform | Typical Cost |

|---|---|

| Bookmaker margin | 4–8% |

| Exchange commission | 2–5% |

Because exchange prices are closer to fair probability, participants frequently receive better odds.

Even after commission is applied, the final outcome may still be more favorable.

Liquidity and Market Quality

Exchange pricing advantages depend heavily on liquidity.

In highly liquid markets:

- spreads remain tight

- odds converge toward fair value

- trading costs remain low

In low-liquidity markets:

- spreads widen

- slippage increases

- effective cost may rise

Therefore the benefits of exchange pricing are strongest in popular events with strong participation.

Understanding the Real Cost of Betting

Participants often focus only on visible fees when evaluating betting platforms.

However, the true cost of participation lies in the structure of pricing itself.

Bookmakers charge through margins embedded in odds.

Exchanges charge through commission applied to winnings.

While both models generate revenue, they shape market behavior in very different ways.

For participants seeking transparent pricing and competitive odds, understanding this structural difference is essential.

Because in betting markets, the cost of participation is rarely obvious — it is hidden inside the price.