Français

Français  Deutsch

Deutsch  Español

Español  Italiano

Italiano  Nederlands

Nederlands  Português

Português  Brasileiro

Brasileiro  Ελληνικά

Ελληνικά  Polski

Polski  Română

Română  Svenska

Svenska  Türkçe

Türkçe  Български

Български  हिंदी

हिंदी

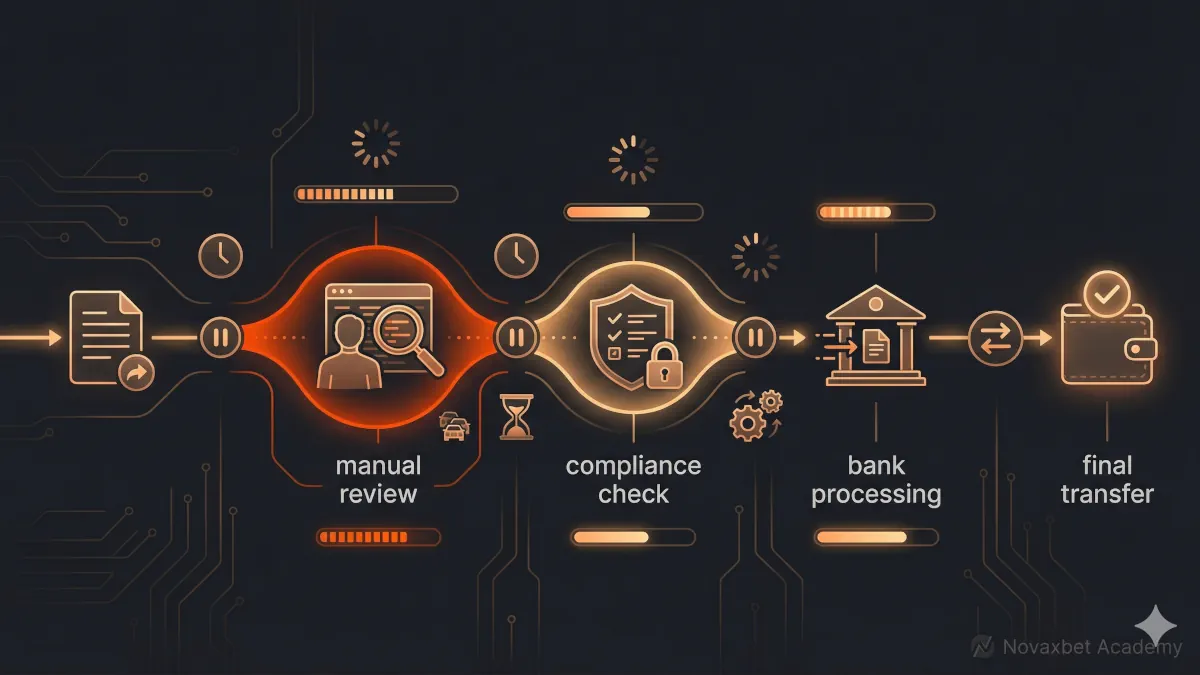

Payout Delays Explained

Why bank payouts can be delayed and what happens during processing.

Novaxbet Editorial •2026-05-11•3 min read

Instant bank transfers are often perceived as free or low-cost, but the actual cost structure can vary depending on banks, payment providers, and transaction types. Understanding these costs helps users make informed decisions and avoid unexpected charges.

Are Instant Bank Transfers Free

Next reading

Instant bank transfers are not always free.

In many cases:

- banks may charge a fee

- platforms may include service costs

- intermediaries may apply processing charges

The total cost depends on how the payment is processed.

Types of Fees in Instant Transfers

Different types of fees can apply.

Bank Fees

Some banks charge for sending or receiving instant payments.

Platform Fees

Payment platforms may include service or processing fees.

Network Fees

Payment schemes may apply infrastructure costs.

Currency Conversion Fees

Fees may apply when transferring between currencies.

Each layer can contribute to the final cost.

Bank Fees Explained

Banks may charge for instant transfers due to:

- real-time processing infrastructure

- priority transaction handling

- risk management systems

Fees can be fixed or percentage-based.

Platform Fees Explained

Payment platforms may add their own charges.

These may include:

- deposit fees

- withdrawal fees

- processing margins

Platforms sometimes bundle fees into the transaction amount.

Hidden Costs to Consider

Not all costs are clearly visible.

Examples include:

- unfavorable exchange rates

- spread between buy and sell prices

- bundled service charges

These can increase the effective cost of the transaction.

Currency Conversion and FX Costs

When payments involve different currencies:

- exchange rates are applied

- additional margins may be included

The total cost is not only the visible fee.

Instant vs Traditional Transfer Costs

Cost differences depend on the system.

Instant transfers:

- may have higher per-transaction fees

- offer faster access to funds

Traditional transfers:

- are often cheaper or free

- take longer to complete

Users trade cost for speed.

Who Pays the Fees

Fees may be paid by different parties.

Possible models:

- sender pays

- receiver pays

- shared cost

This depends on the payment setup.

Free Instant Transfers — When They Exist

Some transfers appear free.

This happens when:

- banks absorb the cost

- platforms subsidize fees

- promotions are applied

Free does not mean no underlying cost exists.

Limits That Affect Fees

Fees may change based on:

- transaction size

- frequency of use

- user account level

Higher-value transactions may have different pricing.

Transparency of Fees

Modern payment systems aim for transparency.

Users may see:

- total cost before confirmation

- breakdown of fees

- exchange rate details

Clear pricing improves user trust.

How to Minimize Costs

Users can reduce fees by:

- comparing providers

- checking exchange rates

- avoiding unnecessary conversions

- choosing appropriate transfer types

Small choices can significantly reduce total cost.

Why Fees Exist in Instant Payments

Fees are linked to:

- infrastructure costs

- real-time processing requirements

- security systems

Instant payments require more resources than traditional ones.

Cost vs Value

Instead of thinking:

“Instant transfers are expensive”

A better perspective is:

“Users pay for speed, convenience, and immediacy”

The value depends on user needs.